Financial Derivatives Pricing as an API

Financial Derivatives Pricing as an API

#API

#Fintech

#GitHub

Financial Derivatives Pricing as an API – QuantLib-powered REST API for bonds, swaps, and credit derivatives

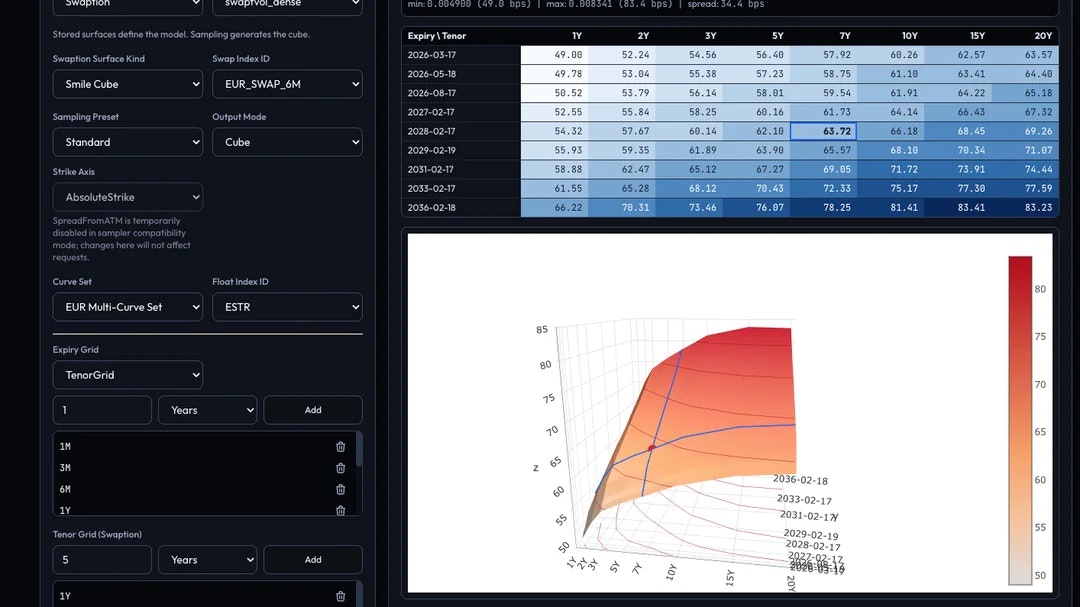

Summary: This API provides production-grade pricing for bonds, swaps, swaptions, FRAs, caps/floors, CDS, and credit derivatives using QuantLib. It offers a REST interface and a web UI for adjusting curves, conventions, and inputs to observe valuation changes.

What it does

It prices various financial derivatives via a REST API or web portal, allowing users to modify parameters and instantly see valuation impacts without coding.

Who it's for

Developers and analysts needing QuantLib-based derivatives pricing without direct programming in C++ or Python.

Why it matters

It simplifies access to QuantLib’s pricing models, enabling experimentation and integration in production environments.